Ornstein–Uhlenbeck process

In mathematics, the Ornstein–Uhlenbeck process (named after Leonard Ornstein and George Eugene Uhlenbeck), is a stochastic process that, roughly speaking, describes the velocity of a massive Brownian particle under the influence of friction. The process is stationary Gauss–Markov process (which means that it is both a Gaussian and Markovian process), and is the only nontrivial process that satisfies these three conditions, up to allowing linear transformations of the space and time variables.[1] Over time, the process tends to drift towards its long-term mean: such a process is called mean-reverting.

The process can be considered to be a modification of the random walk in continuous time, or Wiener process, in which the properties of the process have been changed so that there is a tendency of the walk to move back towards a central location, with a greater attraction when the process is further away from the centre. The Ornstein–Uhlenbeck process can also be considered as the continuous-time analogue of the discrete-time AR(1) process.

Representation via a stochastic differential equation

An Ornstein–Uhlenbeck process, xt, satisfies the following stochastic differential equation:

where , and are parameters and denotes the Wiener process.

The above representation can be taken as the primary definition of an Ornstein–Uhlenbeck process[1] or sometimes also mentioned as the Vasicek model.[2]

Fokker–Planck equation representation

The probability density function ƒ(x, t) of the Ornstein–Uhlenbeck process satisfies the Fokker–Planck equation

![{\frac {\partial f}{\partial t}}=\theta {\frac {\partial }{\partial x}}[(x-\mu )f]+{\frac {\sigma ^{2}}{2}}{\frac {\partial ^{2}f}{\partial x^{2}}}](../I/m/e056324841648bde2e9b0bcbaf82458c4b2e2489.svg)

The Green function of this linear parabolic partial differential equation, taking and for simplicity, and the initial condition consisting of a unit point mass at location is

![f(x,t)={\sqrt {\frac {\theta }{2\pi D(1-e^{-2\theta t})}}}\exp \left\{{\frac {-\theta }{2D}}\left[{\frac {(x-ye^{-\theta t})^{2}}{1-e^{-2\theta t}}}\right]\right\}](../I/m/48718983356ca9410f07b5bba3f27bdb5bce22c8.svg)

The stationary solution of this equation is the limit for time tending to infinity which is a Gaussian distribution with mean and variance

Application in physical sciences

The Ornstein–Uhlenbeck process is a prototype of a noisy relaxation process. Consider for example a Hookean spring with spring constant whose dynamics is highly overdamped with friction coefficient . In the presence of thermal fluctuations with temperature , the length of the spring will fluctuate stochastically around the spring rest length ; its stochastic dynamic is described by an Ornstein–Uhlenbeck process with:

where is derived from the Stokes–Einstein equation for the effective diffusion constant.

In physical sciences, the stochastic differential equation of an Ornstein–Uhlenbeck process is rewritten as a Langevin equation

where is white Gaussian noise with

At equilibrium, the spring stores an average energy in accordance with the equipartition theorem.

Application in financial mathematics

The Ornstein–Uhlenbeck process is one of several approaches used to model (with modifications) interest rates, currency exchange rates, and commodity prices stochastically. The parameter represents the equilibrium or mean value supported by fundamentals; the degree of volatility around it caused by shocks, and the rate by which these shocks dissipate and the variable reverts towards the mean. One application of the process is a trading strategy known as pairs trade.[3][4][5]

Mathematical properties

The Ornstein–Uhlenbeck process is an example of a Gaussian process that has a bounded variance and admits a stationary probability distribution, in contrast to the Wiener process; the difference between the two is in their "drift" term. For the Wiener process the drift term is constant, whereas for the Ornstein–Uhlenbeck process it is dependent on the current value of the process: if the current value of the process is less than the (long-term) mean, the drift will be positive; if the current value of the process is greater than the (long-term) mean, the drift will be negative. In other words, the mean acts as an equilibrium level for the process. This gives the process its informative name, "mean-reverting." The stationary (long-term) variance is given by

The Ornstein–Uhlenbeck process is the continuous-time analogue of the discrete-time AR(1) process.

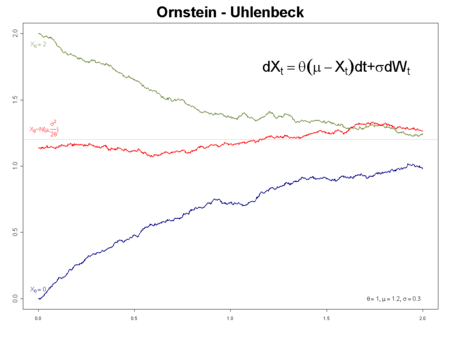

blue: initial value a = 0 (a.s.)

green: initial value a = 2 (a.s.)

red: initial value normally distributed so that the process has invariant measure

Solution

This stochastic differential equation is solved by variation of parameters.. Changing variable

we get

![{\displaystyle {\begin{aligned}df(x_{t},t)&=\theta \,x_{t}\,e^{\theta t}\,dt+e^{\theta t}\,dx_{t}\\[6pt]&=e^{\theta t}\theta \,\mu \,dt+\sigma \,e^{\theta t}\,dW_{t}.\end{aligned}}}](../I/m/871e0ae642c2661631c788771dbe36e9b0a29027.svg)

Integrating from 0 to t we get

whereupon we see

Formulas for moments of nonstationary processes

From this representation, the first moment is given by (assuming that x0 is a constant)

The Itō isometry can be used to calculate the covariance function by

![{\displaystyle {\begin{aligned}\operatorname {cov} (x_{s},x_{t})&=E[(x_{s}-E[x_{s}])(x_{t}-E[x_{t}])]\\&=E\left[\int _{0}^{s}\sigma e^{\theta (u-s)}\,dW_{u}\int _{0}^{t}\sigma e^{\theta (v-t)}\,dW_{v}\right]\\&=\sigma ^{2}e^{-\theta (s+t)}E\left[\int _{0}^{s}e^{\theta u}\,dW_{u}\int _{0}^{t}e^{\theta v}\,dW_{v}\right]\\&={\frac {\sigma ^{2}}{2\theta }}\,e^{-\theta (s+t)}(e^{2\theta \min(s,t)}-1)\\&={\frac {\sigma ^{2}}{2\theta }}\left(e^{-\theta |t-s|}-e^{-\theta (t+s)}\right).\end{aligned}}}](../I/m/30f00901b6407966e9441d0b70ba7e2b134fbc85.svg)

Alternative representation for nonstationary processes

It is also possible (and often convenient) to represent xt (unconditionally, i.e. as ) as a scaled time-transformed Wiener process :

or conditionally (given x0) as

The time integral of this process can be used to generate noise with a 1/ƒ power spectrum.

Scaling limit interpretation

The Ornstein–Uhlenbeck process can be interpreted as a scaling limit of a discrete process, in the same way that Brownian motion is a scaling limit of random walks. Consider an urn containing blue and yellow balls. At each step a ball is chosen at random and replaced by a ball of the opposite colour (equivalently, a ball chosen uniformly at random changes color). Let be the number of blue balls in the urn after steps. Then converges in law to an Ornstein–Uhlenbeck process as tends to infinity.

![{\frac {X_{[nt]}-n/2}{\sqrt {n}}}](../I/m/6f0a36af1442653873ecad48c492eb9cb51dee62.svg)

Generalizations

It is possible to extend Ornstein–Uhlenbeck processes to processes where the background driving process is a Lévy process (instead of a simple Brownian motion). These processes are widely studied by Ole Barndorff-Nielsen and Neil Shephard, and others.

In addition, in finance, stochastic processes are used the volatility increases for larger values of . In particular, the CKLS (Chan–Karolyi–Longstaff–Sanders) process[6] with the volatility term replaced by can be solved in closed form for or 1, as well as for , which corresponds to the conventional OU process.

See also

- The Vasicek model of interest rates is an example of an Ornstein–Uhlenbeck process.

- Short rate model – contains more examples.

Notes

- 1 2 Doob 1942

- ↑ Björk, Tomas. Arbitrage Theory in Continuous Time (3 ed.). Oxford University Press. pp. 375, 381. ISBN 978-0-19-957474-2.

- ↑ Mahdavi Damghani, Babak (2013). "The Non-Misleading Value of Inferred Correlation: An Introduction to the Cointelation Model". Wilmott. 2013 (1): 50–61. doi:10.1002/wilm.10252.

- ↑ Advantages of Pair Trading: Market Neutrality

- ↑ An Ornstein-Uhlenbeck Framework for Pairs Trading

- ↑ Chan et al. (1992)

References

- Bibbona, E.; Panfilo, G.; Tavella, P. (2008). "The Ornstein-Uhlenbeck process as a model of a low pass filtered white noise". Metrologia. 45 (6): S117–S126. doi:10.1088/0026-1394/45/6/S17.

- Chan, K. C.; Karolyi, G. A.; Longstaff, F. A.; Sanders, A. B. (1992). "An empirical comparison of alternative models of the short-term interest rate". Journal of Finance. 47 (3): 1209–1227. doi:10.1111/j.1540-6261.1992.tb04011.x.

- Doob, J. L. (1942). "The Brownian movement and stochastic equations". Annals of Mathematics. 43 (2): 351–369. doi:10.2307/1968873. JSTOR 1968873.

- Gillespie, D. T. (1996). "Exact numerical simulation of the Ornstein–Uhlenbeck process and its integral". Phys. Rev. E. 54 (2): 2084–2091. doi:10.1103/PhysRevE.54.2084. PMID 9965289.

- Risken, H. (1989). The Fokker–Planck Equation: Method of Solution and Applications. New York: Springer-Verlag. ISBN 0387504982.

- Uhlenbeck, G. E.; Ornstein, L. S. (1930). "On the theory of Brownian Motion". Phys. Rev. 36: 823–841. doi:10.1103/PhysRev.36.823.

External links

- Review of Statistical Arbitrage, Cointegration, and Multivariate Ornstein-Uhlenbeck, Attilio Meucci

- A Stochastic Processes Toolkit for Risk Management, Damiano Brigo, Antonio Dalessandro, Matthias Neugebauer and Fares Triki

- Simulating and Calibrating the Ornstein–Uhlenbeck process, M.A. van den Berg

- Maximum likelihood estimation of mean reverting processes, Jose Carlos Garcia Franco

- "Interactive Web Application: Stochastic Processes used in Quantitative Finance".