History of pawnbroking

- This history is partially outdated for developments in the 20th century

The history of pawnbroking began in the earliest ages of the world. Lending money on portable security is one of the oldest professions.

Mosaic law

The Mosaic Law struck at the root of pawnbroking as a profitable business, since it forbade the taking of interest from a poor borrower, while no Jew was to pay another for timely accommodation. Jews would, however, lend money at interest to gentiles. Until the Protestant Reformation, Christians were likewise forbidden to lend to each other at interest. They too have done so and continue to do so against biblical principle.

Franciscans

In spite of early church prohibitions against usury, there is some evidence that the Franciscans were permitted to begin the practice as an aid to the poor, but it remains a question how much they profited on it.

China

The earliest pawnbrokers were in the 5th Century and were established, owned, and operated by Buddhist monasteries; only later did they become more widely seen in society. There were many terms to describe them. The word changshengku (long-life treasuries) originally referred to Buddhist monasteries in general. Other terms included jifupu (seen in Tang texts), didangku (used in the Song periods), and jiedianku (Yuan period). During the Southern Song dynasty, wealthy laypeople would sometimes form partnerships with Buddhist monasteries and open pawnshops (in doing so they also managed to avoid certain property taxes from which monasteries were sometimes exempt). For example, a 1202 memorial records the practice of ten people coming together to form an association known as a ju, which would then back the establishment of a pawnshop in a monastery."[1]

Greece and Rome

Both Greece and Rome were as familiar with the operation of pawning as the modern poor all the world over; indeed, from the Roman jurisprudence most of the contemporary law on the subject is derived. The chief difference between Roman and English law is that under Roman law certain things, such as wearing apparel, furniture, and instruments of tillage, could not be pledged, whereas there is no such restriction in English legislation. The emperor Augustus converted the surplus arising to the state from the confiscated property of criminals into a fund from which the state lent money without interest to those who pledged valuables equal to double the amount borrowed.

Medieval Europe

In Italy, but in more modern times, the pledge system that became almost universal on the continent of Europe arose. In its origin that system was purely benevolent, the early "monts de piete" established by the authority of the popes lending money to the poor only, without interest, on the sole condition of the advances being covered by the value of the pledges. This was virtually the Augustan system, but it is obvious that an institution that costs money to manage and derives no income from its operations must either limit its usefulness to the extent of the voluntary support it can command, or must come to a speedy end.

In 1198 something of the kind was started at Freising in Bavaria.

In 1350 a similar endeavour was made at Salins in Franche-Comté, where interest at the rate of 7½% was charged.

Nor was England backward, for in 1361 Michael Northbury, or de Northborough, bishop of London, bequeathed 1000 silver marks for the establishment of a free pawnshop.

These primitive efforts, like the later Italian ones, all failed. The Vatican was therefore constrained to allow the Sacri monti di pietà (satisfactory derivation of the phrase has yet been suggested) to charge sufficient interest to their customers to enable them to pay for expenses. Thereupon a learned and tedious controversy arose upon the lawfulness of charging interest, which was only finally set at rest by Pope Leo X, who in the tenth sitting of the First Council of the Lateran, declared that the pawnshop was a lawful and valuable institution, and threatened with excommunication those who should presume to express doubts on the subject. The Council of Trent inferentially confirmed this decision, and at a somewhat later date we find St Charles Borromeo counselling the establishment of state or municipal pawnshops.

Long before this, however, monti di pietà commonly charged interest for loans in Italy. The date of their establishment was not later than 1464, when the earliest of which there appears to be any record in that country—it was at Orvieto—was confirmed by Pius II. Three years later another was opened at Perugia by the efforts of two Franciscans, Barnabus Interamnensis and Fortunatus de Copolis. They collected the necessary capital by preaching, and the Perugian pawnshop was opened with such success that there was a substantial balance of profit at the end of the first year.

The Dominicans endeavoured to preach down the lending-house, but without avail. Viterbo obtained one in 1469, and Sixtus IV confirmed another to his native town in Savona in 1479.

After the death of Brother Barnabus in 1474, a strong impulse was given to the creation of these establishments by the preaching of another Franciscan, Father Bernandino di Feltre, who was in due course canonized. By his efforts monti di pietà were opened at Assisi, Mantua, Parma, Lucca, Piacenza, Padua, Vicenza, Pavia and a number of places of less importance.

At Florence the veiled opposition of the municipality and the open hostility of the Jews prevailed against him, and it was reserved to Savonarola, a Dominican, to create the first Florentine pawnshop, after the local theologians had declared that there was no sin, even venial, in charging interest. The readiness of the popes to give permission for pawnshops all over Italy, makes it the more remarkable that the papal capital possessed nothing of the kind until 1539, and even then owed the convenience to a Franciscan.

From Italy the pawnshop spread gradually all over Europe. Augsburg adopted the system in 1591, Nuremberg copied the Augsburg regulations in 1618, and by 1622 it was established at Amsterdam, Brussels, Antwerp and Ghent. Madrid followed suit in 1705, when a priest opened a charitable pawnshop with a capital of fivepence taken from an alms-box.

Later

- Below are historical paragraphs on various countries from the 1911 Encycylopaedia Britannica, which ends in the early 20th century, and are therefore probably not true for the 20th century.

Britain and Ireland

In England the pawnbroker, like so many other distinguished personages, came in with William the Conqueror. Yet, despite the valuable services the class rendered, not infrequently to the Crown itself, the usurer was treated with studied cruelty. Sir Walter Scott's Isaac of York was no mere creation of fiction. These barbarities began, by diminishing the number of Jews in the country, long before Edward's decree of banishment, to make it worth the while of the Lombard merchants to settle in England. In 1338 Edward III pawned his jewels to the Lombards to raise money for his war with France. An equally great king Henry V did much the same in 1415.

Under Henry VII

The Lombards were not a popular class, and Henry VII harried them a good deal. In the very first year of James I's reign an Act against Brokers was passed and remained on the statute-book until Queen Victoria had been 35 years on the throne. It was aimed at counterfeit brokers, of whom there were then many in London. This type of broker was evidently regarded as a mere receiver of stolen goods, for the act provided that no sale or pawn of any stolen jewels, plate or other goods to any pawnbroker in London or Westminster or Southwark shall alter the property therein, and that pawnbrokers refusing to produce goods to their owner from whom stolen shall forfeit double the value.

Under Charles I

In the time of Charles I another act made it clear that the pawnbroker was not deemed a respectable or trustworthy person. Nevertheless, a plan was mooted for setting that king up in the business. The Civil War was approaching and supplies were badly needed, when a too ingenious Royalist proposed the establishment of a state pawnhouse. The preamble of the scheme recited how "the intolerable injuries done to the poore subjects by brokers and usurers that take 30, 40, 50, 60, and more in the hundredth, may be remedied and redressed, the poor thereby greatly relieved and eased, and His Majestie much benefited". That the king would have been much benefited is obvious, since he was to enjoy two-thirds of the profits, while the working capital of £100,000 was to be found by the city of London. The reform of what Shakespeare calls "broking pawn" was in the air at that time, although nothing ever came of it, and in the early days of the commonwealth it was proposed to establish a kind of "mont de pieté". The idea was emphasized in a pamphlet of 1651 entitled "Observatsons manifesting the Conveniency and Commodity of Mount Pieteyes, or Public Bancks for Relief of the Poor or Others in Distress, upon Pawns". No doubt many a ruined cavalier would have been glad enough of some such means of raising money, but this radical change in the principles of English pawnbroking was never brought about. It is said that the Bank of England, under its charter, has power to establish pawnshops; and we learn from A Short History of the Bank of England, published in its very early days, that it was the intention of the directors, for the ease of the poor, to institute a Lombard for small pawns at a penny a pound interest per month (= 5% per year).[2]

1600 to 1800

Throughout both the 17th and 18th centuries the general suspicion of the pawnbroker appears to have been only too well founded. During George II's reign Fielding wrote a book Amelia; references in that book seem to show that, taken in the mass, Fielding was not a very scrupulous tradesman. Before about that time it was customary for publicans to lend money on pledges so their customers could drink, but the practice was at last stopped by Act of Parliament.

Also, respect for the honesty of pawnbroking was harmed by the Charitable Corporation's actions, during which affair it was pointed out that pawnbroking, by affording an easy method of raising money upon valuables, encourages dishonesty, by:-

- Furnishing the thief and pickpocket with a better opportunity to sell their stolen goods.

- Letting a man intending to become bankrupt buy goods on credit and dispose of them for ready money, defrauding his creditors.

Pawnbroker's licence law, 1785

The pawnbroker's licence dates from 1785, the duty being fixed at £10 in London and £5 in the country; and at the same time the interest chargeable was settled at ½% per Modern month, the duration of loans being confined to one Regulations year. Five years later the interest on advances in England between 2 and 10 was raised to 15%.

The modern history of legislation affecting pawnbroking begins, however, in 1800, when the act of ~9 & 40 Geo. III. c. 99 (1800) was passed, in great measure by the influence of Lord Eldon, who never made any secret of the fact that, when he was a young barrister without briefs, he had often been indebted to the timely aid of the pawnshop. The pawnbrokers were grateful, and for many years after Lord Eldon's death they continued to drink his health at their trade dinners. The measure increased the rate of interest to 1.6666666% per month, which is 20% a year unless unpaid interest adds to the debt. Loans were to be granted for a year, but pledges might be redeemed up to fifteen months, and the first week of the second month was not to count for interest.

The act worked well, on the whole, for 75 years, but it was amended 3 times:-

- 1815: Licence duties were raised to £15 for London and £7.50 for the country.

- 1840: An Act of Parliament abolished the reward to the common informer for reporting illegal rates of interest.

- 1860: The pawnbroker was empowered to charge a halfpenny (= about 0.2 p) for the pawn-ticket when the loan was under five shillings (= 25p).

As time went on, however, the main provisions of the act of 1800 were found to be very irksome, and the Pawnbrokers National Association and the Pawnbrokers Defence Association worked hard to obtain a liberal revision of the law. It was argued that the usury laws had been abolished for the whole of the community except only for the pawnbroker who advanced less than £10. The limitations of the act of 1800 interfered so considerably with the pawnbrokers' profits that, it was argued, they could not afford to lend money on bulky articles needing extensive storage room. In 1870 the House of Commons appointed a Select Committee on Pawnbrokers, and it was stated in evidence before that body that in the previous year 207,780,000 pledges were lodged, of which between thirty and forty millions were lodged in London. The average value of pledges appeared to be about 4s., and it was claimed that the proportion of articles pawned dishonestly was found to be only 1 in 14,000. Later official statistics show that of the forfeited pledges sold in London less than 20 per million are claimed by the police.

Pawnbroker's licence law, 1872

The result of the Select Committee was the Pawnbrokers Act of 1872, which repealed, altered and consolidated all previous legislation on the subject, and is still the measure which regulates the relations between the public and pawnbrokers. It was based mainly on the Irish law passed by the Union Parliament. It put an end to the old irritating restrictions, and reduced the annual tax in London from £15 to the £7.50 paid in the provinces. By the provisions of the Act (which does not affect loans above £10):-

- A pledge is redeemable within one year, and seven days of grace added to the year.

- Pledges pawned for £0.50 or under and not redeemed in time become the property of the pawnbroker.

- Pledges above £0.50 are redeemable until sale, which must be by public auction.

- In addition to one halfpenny (= about 0.2 p) for the pawn-ticket (sometimes not charged for very small pawns) the pawnbroker is entitled to charge as interest one halfpenny per month on every 2s. or part of 2s. lent where the loan is under £2, and on every 2s. 6d. where the loan is above £2. (Note: "s." = shilling = 5p.)

- Special contracts may be made where the loan is above £2, at a rate of interest agreed on between lender and borrower.

- These made offences punishable by summary conviction:-

- Unlawful pawning of goods not the property of the pawner.

- Taking in pawn any article from a person under the age of twelve, or intoxicated.

- Taking in pawn any linen or apparel or unfinished goods or materials entrusted to wash, make up, etc.

- A new pawnbroker must produce a magistrate's certificate before he can receive a licence.

- The permit cannot be refused if the applicant gives sufficient evidence that he is a person of good character.

- The word "pawnbroker" must always be inscribed in large letters over the door of the shop.

Elaborate provisions are made to safeguard the interests of borrowers whose unredeemed pledges are sold under the act. Thus the sales by auction may take place only on the first Monday of January, April, July and October, and on the following days should one day not be sufficient. This legislation was, no doubt, favorable to the pawnbroker rather than to the borrower. The annual interest on loans of 2s. had been increased by successive acts of parliament from 6% in 1784 to 25% in 1800, and to 27% in 1860, and re-set at 27% in 1872. The annual interest on a loan of half-a-crown (now 12½p) is now 260%, as compared with 173 in 1860 and 86 in 1784; the extreme point is reached in the case of a loan of 1s. for three days, in which case the interest is at the rate of 1014% per annum.

An English mont de piété was once projected by the Salvation Army, and in 1894 the London County Council considered the practicability of municipal effort on similar lines; but in neither case was anything done.

Scotland and Ireland

The growth of pawnbroking in Scotland, where the law as to pledge agrees generally with that of England, is remarkable.

Early in the 19th century there was only one pawnbroker in Ireland, and in 1833 there were only 52. Even in 1865 there were no more than 312. It is probable that Glasgow and Edinburgh together contain nearly as many as that total. In Ireland the rates for loans are practically identical with those charged in England, but a penny instead of a halfpenny is paid for the ticket. Articles pledged for less than Li must be redeemed within six months, but nine months are allowed when the amount is between 3os. and 2. For sums over 2 the period is a year, as in England. In Ireland, too, a fraction of a month is calculated as a full month for purposes of interest, whereas in England, after the first month, fortnights are recognized. In 1838 there was an endeavour to establish monts de piété in Ireland, but the scheme was so unsuccessful that in 1841 the eight charitable pawnshops that had been opened had a total adverse balance of 5340. By 1847 only three were left, and eventually they collapsed likewise.

United States

The pawnbroker in the United States is, generally speaking, subject to considerable legal restriction, but violations of the laws and ordinances are frequent. Each state has its own regulations, but those of New York and Massachusetts may be taken as fairly representative.

Brokers of pawn are usually licensed by the mayors, or by the mayors and aldermen, but in Boston the police commissioners are the licensing authority. In the state of New York permits are renewable annually on payment of $500, and the pawnbroker must file a surety bond with the Department of Consumer Affairs, in the sum of $10,000. The business is conducted on much the same lines as in England. The rate of interest is 4% per month and the loan is written for a period of 4 months, with an additional 30-day grace period. To enact higher rates is a misdemeanor. Unredeemed pledges may be sold at any time after the legal time for the loan. New York contains one pawnshop to every 12,000 inhabitants. In the state of Massachusetts unredeemed pledges may be sold four months after the date of deposit. The licensing authority may fix the rate of interest, which may vary for different amounts, and in Boston every pawnbroker is bound to furnish to the police daily a list of the pledges taken in during the preceding twenty-four hours, specifying the hour of each transaction and the amount lent.

Major pawnshop chains include Cash America International and First Cash Financial Services, both headquartered in Texas.

Europe

The fact that on the continent of Europe monts de piété are almost invariably either a state or a municipal monopoly necessarily places them upon an entirely different footing from the British pawnshop, but, compared with the English system, the foreign is very elaborate and rather cumbersome. Moreover, in addition to being slow in its operation, it is, generally speaking, based upon the supposition that the borrower carries in his pockets papers testifying to his identity. On the other hand, it is argued that the English borrower of more than 2 is at the mercy of the pawnbroker in the matter of interest, that sum being the highest for which a legal limit of interest is fixed. The rate of interest upon a special contract may be, and often is, high. For the matter of that, indeed, this system of obtaining loans is always expensive, either in actual interest or in collateral disadvantages, whether the lender be a pawnbroker intent upon profit, or the official of a mont de pit. In Paris the rate charged is 7%, and even then the business is conducted at a loss except in regard to long and valuable pledges. Some of the French provincial rates are as high as 12%, but in almost every case they are less than they were prior to the legislation of 1851 and 1852. The French establishments can only be created by decree of the president of the Republic, with the consent of the local conseil communal. In Paris the prefect of the Seine presides over the business; in the provinces the mayor is the president. The administrative council is drawn one-third each from the conseil communal, the governors of charitable societies, and the townspeople. A large proportion of the capital required for conducting the institutions has to be raised by loan, while some part of the property they possess is the product of gifts and legacies. The profits of the Paris mont de pit are paid over to the Assistance Publique, the comprehensive term used by France to indicate the body of charitable foundations. Originally this was the rule throughout France, but now many of them are entirely independent of the charitable institutions. Counting the head office, the branches and the auxiliary shops, the Paris establishment has its doors open in some fifty or sixty districts; but the volume of its annual business is infinitely smaller than that transacted by the London pawnbrokers. The amount to be advanced by a municipal pawnshop is fixed by an official called the commissaire-priseur, who is compelled to load the scales against the borrower, since, should the pledge remain unredeemed and be sold for less than was lent upon it, he has to make good the difference. This official is paid at the rate of 3/4% upon loans and renewals, and 3% on the amount obtained by the sales of forfeited pledges. This is obviously the weakest part of the French system. The Paris mont de pit undertakes to lend four-fifths of the intrinsic value of articles made from the precious metals, and two-thirds of that of other articles. The maximum and minimum that may be advanced are also fixed. The latter varies in different parts of the country from one to three francs, and the former from a very small sum to the 10,000 francs that is the rule in Paris. Loans are granted for twelve months with right of renewal, and unredeemed pledges may then be sold by auction, but the proceeds may be claimed by the borrower at any time within three years. Pledges may be redeemed by instalments.

Somewhere between forty and fifty French towns possess municipal pawnshops, a few of which, like those of Grenoble and Montpellier, having been endowed, charge no interest. Elsewhere the rate varies from nil in some towns, for very small pledges, to 10%. The constant tendency throughout France has been to reduce the rate. The great establishment in Paris obtains part of its working capital reserves and surplus forming the balance by borrowing money at a rate varying from 2 to 3% according to the loan term (duration). Under a law passed in 18gf the Paris mont de pit makes advances upon securities at 6%, plus a duty of 5 centimes upon every hundred francs. The maximum that can be lent in this way is 20. Up to 80% is lent on the face value of government stock and on its own bonds, and 75% upon other securities; but 60% only may be advanced on railway shares. These advances are made for six months. Persons wishing to borrow a larger sum than sixteen francs from the Paris mont de pit have to produce their papers of identity. In every case a numbered metal check is given to the customer, and a duplicate is attached to the article itself. The appraising clerks decide upon the sum that can be lent, and the amount is called out with the number. If the borrower is dissatisfied he can take away his property, but if he accepts the offer he has to give I till particulars of his name, address and occupation. Experts calculate that every transaction that involves less than twenty-two francs results in a loss to the Paris mont de pit—only those that exceed eighty-five francs are profitable. The average loan is under thirty francs.

The Netherlands and Belgium

Borrowing money on the security of deposited goods has been the subject of minute regulations in the Low Countries from as far back as the year 1600.

The archdukes Albert and Isabella, governors of the Spanish Netherlands under Philip III, reduced the lawful rate of interest from 32 3/4 to 21 3/4%; but since extortion continued they introduced the mont de pit in 1618, and, as we have already seen, in the course of a dozen years the institution was established in all the populous Belgian towns, with one or two exceptions. The interest chargeable to borrowers was fixed originally at 15%, but was shortly afterwards reduced, to be again increased to nearly the old level. Meanwhile, various towns possessed charitable funds for gratuitous loans, apart from the official institutions. Shortly after the mont de pit was introduced in the Spanish provinces, the prince-bishop of Liège, Ferdinand of Bavaria, followed the example set by the archdukes. He ordained that the net profits were to accumulate, and the interest upon the fund to be used in reduction of the charges. The original rate was 15%, when the Lombard money-lenders had been charging 43; but the prince-bishops monts de pit were so successful that for many years their rate of interest did not exceed 5% - it was, indeed, not until 1788 that it was increased by one-half. These flourishing institutions, along with those in Belgium proper, were ruined by the French Revolution. They were, however, re-established under French dominion, and for many years the laws governing them were constantly altered by the French, Dutch and Belgian governments in turn. The whole subject is now regulated by a law of 1848, supplemented by a new constitution for the Brussels mont de pit dating from 1891.

The working capital of these official pawnshops is furnished by charitable institutions or the municipalities, but the Brussels one possesses a certain capital of its own in addition. The rate of interest charged in various parts of the country varies from 4 to 16%, but in Brussels it is usually less than half the maximum. The management is very similar to that of the French monts de pit, but the arrangements are much more favorable to the borrower. The ordinary limit of loans is I2o. In Antwerp there is an anonymous pawnshop, where the customer need not give his name or any other particulars. In the Netherlands private pawhbrokers flourish side by side with the municipal Banken van Leening, nor are there any limitations upon the interest that may be charged. The rules of the official institutions are very similar to those of the monts de pit in the Latin countries, and unredeemed pledges are sold publicly 15 months after being pawned. A large proportion of the advances are made upon gold and diamonds; workmen's tools are not taken in pledge, and the amount lent varies from 8d. upwards. On condition of finding such sum of money as may be required for working capital over and above loans from public institutions, and the caution money deposited by the city officials, the municipality receives the profits.

Germany

Pawnbroking in Germany is conducted at once by the state, by the municipalities, and by private enterprise; but of all these institutions the state loan office in Berlin is the most interesting. It dates from 1834, and the working capital was found, and still continues to be in part provided, by the Prussian State Bank. The profits are invested, and the interest devoted to charitable purposes. The maximum and minimum rates of interest are fixed, but the rate varies, and often stands at about 12%. Two-thirds of the estimated value is the usual extent of a loan; four-fifths is advanced on silver, and five-sixths on fine gold. State and municipal bonds may be pledged up to a maximum of L150, the advance being 80% of the value, and a fixed interest of 6% is charged upon these securities. The values are fixed by professional valuers, who are liable to make good any loss that may result from over-estimation. The bulk of the loans are under 5, and the state office is used less by the poor than by the middle classes. Loans run for six months, but a further six months' grace is allowed for redemption before the article pledged can be sold by auction. The net annual profit usually amounts to little more than I % upon the capital employed. Pawnbroking laws of Austria-Hungary are similar to those of England. Free trade exists, and the private trader, who does most of the business, must obtain a government concession and deposit caution-money from 80 to 800, according to the size of the town. He must, however, compete with the monts de pit or Versatzaemter, which are sometimes municipal and sometimes state institutions. The chief of these is the imperial pawn office of Vienna, which was founded with charitable objects by the emperor Joseph I in 1707, and one-half of the annual surplus has still to be paid over to the Vienna poor fund. Here, as in Berlin, the profits are relatively small. Interest is charged at the uniform rate of 10%, which is calculated in two-week periods, however speedily redemption may follow upon pawning. For small loans varying from two to three kronen, 5% only is charged. The Hungarian state and municipal institutions appear, on the whole, to compete somewhat more successfully with the private firms than is the case in Vienna.

Italy

In Italy, the country of origin of the mont de piété, the institution still flourishes. It is, as a rule, managed by a committee or commission, and the regulations follow Italy pretty closely the lines of the one in Rome, which never lends less than fod. or more than 40. Four-fifths of the value is lent upon gold, silver and jewels, and two-thirds upon other articles. The interest, which is reckoned monthly, varies with the amount of the loan from 5 to 7%, but no interest is chargeable upon loans up to 5 lire. A loan runs for six months, and may be renewed for similar periods up to a maximum of five years. If the renewal does not take place within a fortnight of the expiration of the ticket, the pledge is sold, any surplus there may be being paid to the pawner. When more than 10 lire is lent there is a charge of 1% for the ticket. Agencies of the mont de pit are scattered about Rome, and carry on their business under the same rules as the central office, with the disadvantage to the borrower that he has to pay an agents fee. The amount to be advanced by a municipal pawnshop is fixed by an official called the commissaire-priseur, who is compelled to load the scales against the borrower, since, should the pledge remain unredeemed and be sold for less than was lent upon it, he has to make good the difference. This official is paid at the rate of 3/4% upon loans and renewals, and 3% on the amount obtained by the sales of forfeited pledges. The borrower has to pay an agents fee of 2%, which is deducted from the loan. Private pawnshops also exist in Italy, under police authority; but they charge very high interest.

France

The institution was very slow in obtaining a footing in France. It was adopted at Avignon in 1577, and at Arras in 1624. The doctors of the once powerful Sorbonne could not reconcile themselves to the lawfulness of interest, and when a pawnshop was opened in Paris in 1626, it had to be closed within a year. Then it was that Jean Boucher published his Défense des monts de piété in favor of pawnbroking. Marseilles obtained one in 1695; but it was not until 1777 that the first mont de pit was founded in Paris by royal patent. Statistics for the first few years of its existence show that in the twelve years between 1777 and the Revolution, the average value of the pledges was 42 francs 50 centimes, which is double the present average. The interest charged was 10% per annum, and large profits were made upon the sixteen million livres that were lent every year. The National Assembly, in an evil moment, destroyed the monopoly of the monti de pietà, but it struggled on until 1795, when the competition of the money-lenders compelled it to close its doors. So great, however, were the extortions of the usurers that the people began to clamour for its reopening, and in July 1797 it recommenced business with a fund of ~20,000 found by five private capitalists. At first it charged interest at the rate of 36% per annum, which was gradually reduced, the gradations being 30, 24, 18, 15, and finally 12% in 1804. In i806 it fell to 9%, and in 1887 to 7%. In 1806 Napoleon I re-established its monopoly, while Napoleon III, as prince-president, regulated it by new laws that are still in force. In Paris the pledge-shop is, in effect, a department of the administration; in the French provinces it is a municipal monopoly; and this remark holds good, with modifications, for most parts of the continent of Europe.

The Paris mont de piété undertakes to lend four-fifths of the intrinsic value of articles made from the precious metals, and two-thirds of that of other articles. The maximum and minimum that may be advanced are also fixed. The latter varies in different parts of the country from one to three francs, and the former from a very small sum to 10,000 francs that is the rule in Paris. Loans are granted for twelve months with right of renewal, and unredeemed pledges may then be sold by auction, but the proceeds may be claimed by the borrower at any time within three years. Pledges may be redeemed by instalments.

Spain

The monts de piété in Spain have for a generation past been inseparably connected with the savings banks. We have already seen that the institution owes its origin in that country to the charitable exertions of a priest who charged no interest, and the system grew until in 1840, a century after his death, the mont de pit began to receive the sums deposited in the savings bank, which had just been established, for which it paid 5% interest. In 1869 the two institutions were united. This official pawnshop charges 6% upon advances for periods varying from four to twelve months, according to the nature of the article pledged, and a further months grace is allowed before the pledges are sold by auction. Private pawnbrokers are also very numerous, especially in Madrid; but their usual charges amount to about 60% per annum. They appear, however, to derive advantage from making larger advances than their official rivals, and from doing business during more convenient hours. In Portugal the monte pio is an amalgamation of bank, benefit society and pawnshop. Its business consists chiefly in lending money upon marketable securities, but it also makes advances upon plate, jewelry and precious stones, and it employs officially licensed valuers. The rate of interest varies with the bank rate, which it slightly exceeds, and the amount advanced upon each article is about three-fourths of its certified value. There is in Portugal a second class of loan establishment answering exactly to the English pawnshop. The pawnbroker is compelled to deposit a sum, in acceptable securities, equal to the capital he proposes to embark, and the register of his transactions must be submitted quarterly to the chief of the police for examination. As regards small transactions, there appears to be no legal limit to the rate of interest. The sale of unredeemed pledges is governed by the law affecting the monte pio geral.

Russia

In imperial Russia the state maintained two pawnbroking establishments, one at St Petersburg and the other at Moscow, but only articles of gold and silver, precious stones and ingots of the precious metals are accepted by them. Advances are made upon such securities at 6% per annum, and the amounts of the loans are officially limited. Loans run for twelve months, with a months grace before unredeemed pledges are put up to auction. The bulk of this class of business in Russia was, however, conducted by private companies, which advance money upon all descriptions of movable property except stocks and shares. The interest charged was not allowed to exceed I % per month, but there is an additional charge of 4% per month for insurance and safe keeping. The loan runs for a year, with two months grace for redemption before sale. There were also pawnshops conducted by individuals, who find it very difficult to compete with the companies. These shops can only be opened by a police permit, which runs for five years, and security, varying from 100 to 700, has to be deposited; 2% per month is the limit of interest fixed, and two months grace is allowed for redemption after the period for which an article is pledged.

Denmark

Pawnbroking in Denmark dates from 1753, when the Royal Naval Hospital was granted the monopoly of advancing money on pledges and of charging higher interest than the law permitted. The duration of a loan is three months, renewals being allowed. The old law was extended in 1867, and now all pawnbrokers have to be licensed by the municipalities and to pay a small annual licence fee. The rate of interest varies from 6 to 12% according to the amount of the loan, which must not be less than 7d., and unredeemed pledges must be sold by auction.

Sweden

Sweden has no statutes specifically aimed at pawnbroking, with the exception of a proclamation by the governor of Stockholm that prohibits lending money on articles suspected being stolen. Individuals still carry on the business on a small scale, but the bulk of it is now conducted by companies, which give general satisfaction. For many years Stockholm had a municipal establishment that charged 10% for loans paid out of the city funds. The cost of administration was, however, so great that the establishment suffered an annual loss, and was abolished when, in 1880, a private company called the Pant Aktie Bank 'pawn bond bank' formed to lend money on furniture and wearing apparel at the rate of 3 öre per krona a month, and 2 öre per krona a month on gold, silver and other valuables. A krona, which equals 1s. 14d., contains 100 öre. Some years later an opposition started that charged only half these rates, with the result that the original enterprise reduced its interest to the same level, charging, however, 2 öre per krona per mensem for bulky articles—a figure now usual for pledges of that description. The money is lent for three months, and at the end of five months the pledge, if unredeemed, is sold by auction under very carefully prescribed conditions. In Norway a police licence is required for lending money on pawn where the amount advanced does not exceed 4, 10s. Beyond that sum no licence is necessary, but the interest charged must not exceed such a rate as the king may decide.

Switzerland

The fate of pawnbroking in Switzerland appears to be not very dissimilar from that of the Jew who is fabled to have once started in business at Aberdeen. Nevertheless, the cantons of Bern and Zürich enacted elaborate laws for the regulation of the business. In Zürich the broker must be licensed by the cantonal government, and the permit can be refused only when the applicant is known to be a person undeserving of confidence. Regular books have to be kept, which must be at all times open to the inspection of the police, and not more than 1% interest per month may be charged. A loan runs for six months, and unredeemed pledges may be sold by auction a month after the expiration of the fixed period, and then the sale must take place in the parish in which the article was pledged. No more than two persons at a time have ever been licensed under this law, the business being unprofitable owing to the low rate of interest. In the canton of Bern there were once two pawnbrokers. One died and the other put up his shutters. The Zürich cantonal bank, however, conducts a pawnbroking department, which lends nothing under 4s. or over £40 without the special sanction of the bank commission. Loans must not exceed two-thirds of the trade value of the pledge, but 80% may be lent upon the intrinsic value of gold and silver articles. The establishment makes practically no profit. The Swiss disinclination to go to the pawnshop is, perhaps, accounted for in some measure by the growing number of dealers in second-hand articles, to whom persons in want of ready money sell outright such things as are usually pledged, in the hope of subsequently buying them back. Since, however, the dealer is at liberty to ask his own price for repurchase, the expectation is often illusory, and can usually be fulfilled only upon ruinous terms.

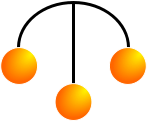

The symbol

The pawnbroker's symbol shows three balls suspended from a bar. The three-ball symbol is attributed to the Medici Family of Florence, Italy, because of its symbolic meaning of Lombard, referring to the Italian province of Lombardy, where pawn shop banking originated under the name of Lombard banking. It is now as well established as anything of the kind can be that the three golden balls, which have for so long been the trade sign of the pawnbroker, were originally the symbol medieval Lombard merchants hung up in front of their houses, and not, as has often been suggested, the arms of the Medici family. It has, indeed, been conjectured that the golden balls were originally three flat yellow effigies of byzants, or gold coins, laid heraldically upon a sable field, but that they were presently converted into balls the better to attract attention.

Most European towns called the pawn shop the "Lombard". The House of Lombard was a banking family in medieval London. According to legend, a Medici employed by Charles the Great slew a giant using three bags of rocks. The three-ball symbol became the family crest. Since the Medicis were so successful in the financial, banking, and money-lending industries, other families also adopted the symbol. Throughout the Middle Ages, coats of arms bore three balls, orbs, plates, discs, coins and more as symbols of monetary success. Pawnbrokers (and their detractors) joke that the three balls mean "Two to one, you won't get your stuff back".

See also

- Mount of piety (Mont de Piété)

Sources and references

This article incorporates text from a publication now in the public domain: Herbermann, Charles, ed. (1913). "article name needed". Catholic Encyclopedia. New York: Robert Appleton.

This article incorporates text from a publication now in the public domain: Herbermann, Charles, ed. (1913). "article name needed". Catholic Encyclopedia. New York: Robert Appleton.